Wall Street has developed a new obsession: can computing power be traded like crude oil? On 12th May, the Chicago Mercantile Exchange (CME) announced a partnership with start-up Silicon Data to launch the world's first futures market linked to GPU price indices. Terry Duffy, CME's chairman, called compute "the new oil of the 21st century." Larry Fink, chief executive of BlackRock, predicted that compute futures would give birth to an entirely new asset class. Around the same time, Architect — an exchange run by Brett Harrison, former president of FTX US — began offering futures contracts based on GPU agreements. On 28th May, Architect went further, acquiring a fully regulated Designated Contract Market (DCM) under the oversight of the Commodity Futures Trading Commission (CFTC) and launching what it describes as a dedicated "AI exchange."

The commercial logic is straightforward. The cost of renting an hour of Nvidia's latest Blackwell chip has doubled since February. Until now, there has been no financial instrument to hedge that price risk. An AI start-up wishing to lock in the cost of GPU capacity twelve months hence had nowhere to turn. Compute futures aim to fill that gap. Data-centre operators could securitise predictable future revenues; AI companies could fix today's price against costs that might double within six months.

When a commodity becomes a financial asset

History offers a cautionary precedent. Crude oil began as an industrial input and ended up as one of the world's most speculative assets. The pattern has repeated itself across natural gas, electricity, grain and carbon credits: derivatives markets grow far larger than the underlying physical trade, and prices decouple from supply and demand. Compute carries an additional hazard that oil does not. Crude has a bedrock of proven, cash-generating end uses — cars, aircraft, chemicals. A significant share of AI compute demand, by contrast, rests on future expectations that have yet to be validated by actual cash flows. The stronger the belief that AI will transform the economy, the higher compute futures prices rise; rising prices reinforce the belief. Run the logic in reverse — if AI monetisation disappoints — and the result could resemble the dotcom collapse of 2000, when technology valuations imploded simultaneously across the board.

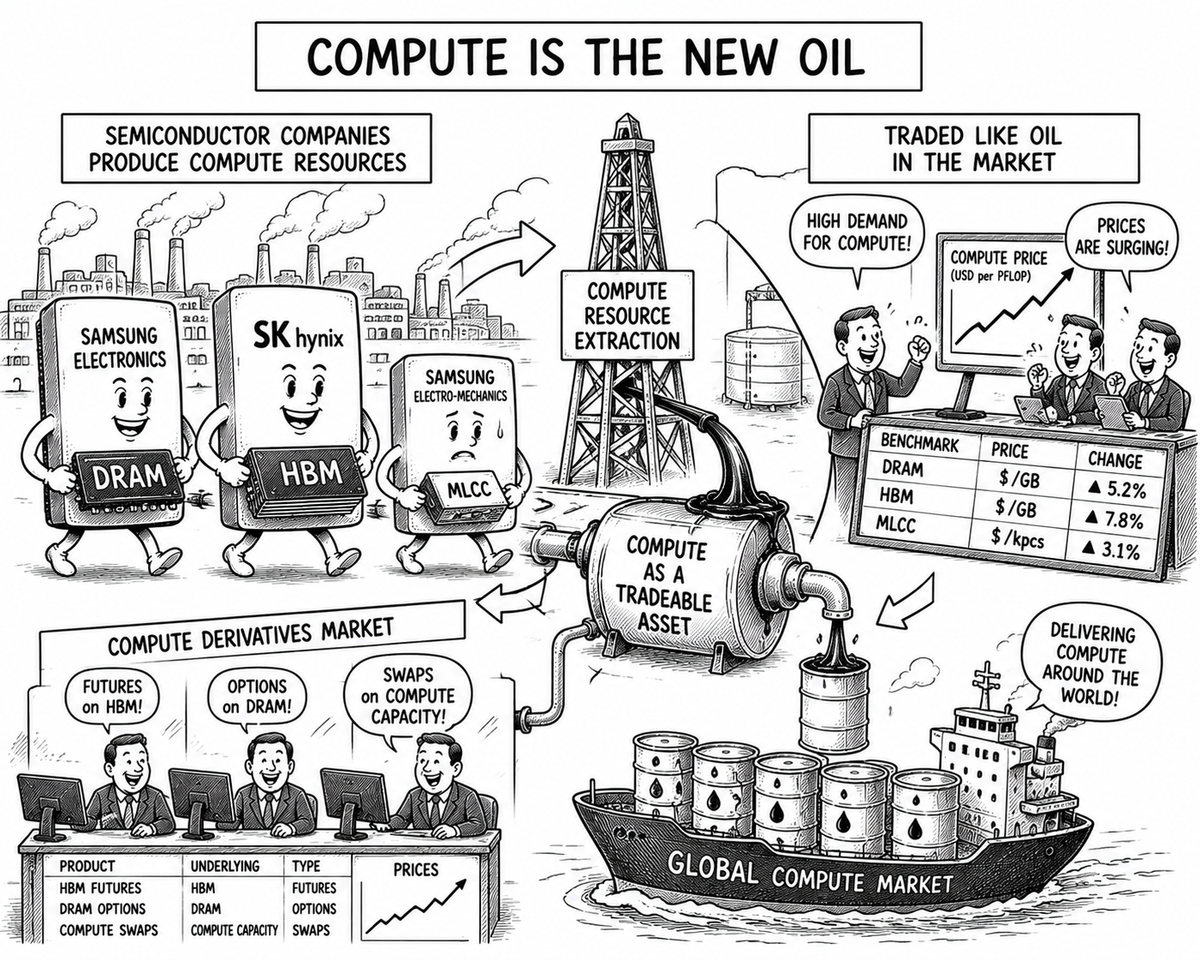

Korea is not a bystander in this drama. Its companies control a substantial share of the global supply of the critical raw materials from which computing power is built: high-bandwidth memory (HBM), DRAM, and a less celebrated but equally indispensable component — the multilayer ceramic capacitor, or MLCC.

HBM and DRAM: absorbing the volatility of compute's engine room

For SK Hynix and Samsung Electronics, the financialisation of compute is an extension of a trend already well under way. An AI server derives its value from the combination of GPUs, HBM, networking equipment and power infrastructure. Of these, HBM has become the fastest-growing bottleneck alongside the GPU itself. Markets already treat the two Korean chipmakers' HBM output as an integral part of the compute supply chain.

If compute futures become firmly established, investor attention will inevitably turn to the cost of producing compute — treating HBM, power and cooling infrastructure as raw-material inputs. Just as rising oil prices lift the share prices of drillers and oilfield-services companies, rising compute prices could amplify earnings expectations for SK Hynix, Samsung Electronics and Micron. This is precisely why markets are already awarding HBM businesses far higher valuation multiples than the traditional DRAM cycle ever warranted. HBM is no longer perceived merely as a memory product; it is being recast as the essential feedstock for the computational capacity that underpins the AI economy.

Yet the reinterpretation brings risks of its own. If speculative capital floods into compute futures in earnest, HBM and DRAM prices could swing wildly regardless of physical supply and demand. Memory prices already lurch from quarter to quarter in response to AI server order cycles. Add a layer of financial derivatives on top, and volatility could increase by another order of magnitude.

MLCC: the overlooked raw material of the compute economy

The least appreciated variable in this picture is Samsung Electro-Mechanics and the humble MLCC. Multilayer ceramic capacitors store electrical charge and release it in stable flows to CPUs and GPUs, ensuring semiconductors operate reliably. A single smartphone contains more than 1,000 of them — they are, in that sense, unremarkable. But an AI server consumes five to ten times as much power as a conventional server, and a single AI server typically requires around 28,000 MLCCs.

What is happening in this market bears a striking resemblance to the early stages of the HBM supply cycle. When news emerged that Murata Manufacturing was considering price increases for AI-grade MLCCs, the shares of both Murata and Samsung Electro-Mechanics jumped sharply. Industry sources report that server customers are demanding volumes that are "realistically impossible" to fulfil, and analysts believe high-specification MLCC supply will remain constrained through at least 2027. One brokerage note observed that investors who lived through the DRAM cycle would find the situation uncomfortably familiar. JP Morgan forecasts that Samsung Electro-Mechanics' MLCC revenues will reach 10.669 trillion won next year, nearly double the 5.198 trillion won recorded last year. Sales of AI server MLCCs are projected to grow 2.4-fold both this year and in 2027 relative to their respective prior years.

Samsung Electro-Mechanics already holds approximately 40% of the AI server MLCC market, but its production lines are running at full capacity. The company has approved an expansion of its Philippine factory, though volume production remains two years away. That structural gap between supply and demand is feeding directly into price increases. One securities firm raised its operating-profit estimates for Samsung Electro-Mechanics by 6% for 2026 and 16% for 2027, arguing that a shift in product mix — less mobile, more AI — would drive a sustained improvement in margins.

A revealing detail emerged from Architect's 28th May announcement. The exchange said it would offer cross-margin products covering not only compute derivatives but also "related inputs such as metals, energy and power." From the outset, in other words, the compute exchange conceives of its market as encompassing the raw materials that go into producing compute, not just compute itself. There is no direct evidence yet that MLCCs would be included under the heading of "metals." But the broader ambition — to financialise the entire AI infrastructure supply chain — is explicit. If HBM can serve as the underlying asset for a memory futures contract, it is reasonable to speculate that MLCCs could eventually be incorporated into a compute-components index. That remains a projection rather than an established fact, but the direction of travel is clear.

The same coin, two sides

For all three companies, the financialisation of compute cuts both ways. The upside is tangible. A functioning compute futures market would make long-term procurement by data-centre operators more predictable, which in turn could accelerate the spread of long-term supply agreements (LTAs) for HBM, DRAM and MLCCs. SK Hynix is already pursuing an LTA strategy; Samsung Electro-Mechanics is already pivoting its product mix toward higher-value server components. Greater price visibility would also allow Korean manufacturers to plan capital expenditure with more confidence.

The downside is equally substantial. If derivatives trading grows far larger than the underlying physical market — the standard pattern in commodity financialisation — prices will begin to track speculative positioning rather than real demand. That volatility would transmit directly to HBM, DRAM and MLCC prices. Korean semiconductor and electronic-components companies currently carry valuations that are heavily dependent on the "AI supercycle" narrative. Should a speculative bubble in compute futures deflate, the damage would flow straight back into those valuations.

The question that matters most

Everything in this analysis converges on a single question: will AI generate the durable, self-sustaining cash flows required to justify its status as permanent economic infrastructure? If it does, compute will establish itself as an enduring asset class alongside oil and electricity, and the Korean companies that supply its raw materials will acquire a new identity as providers of compute feedstock to the world. If AI monetisation falls short of expectations, the compute futures market itself could wither for lack of volume, and the valuation premiums attached to memory and MLCCs would deflate alongside it.

The world stands at the fork in that road. Samsung Electronics, SK Hynix and Samsung Electro-Mechanics are already embedded deep within the supply chain of compute as a commodity. What remains undetermined is whether they will secure the role of stable, indispensable raw-material suppliers — or become the first to absorb the volatility that speculative financialisation invariably produces.

Watch for: regulatory approval and the actual trading launch of the CME-Silicon Data compute futures contract, and the volatility patterns in HBM and server-grade MLCC spot prices once that market opens. If compute futures prices and memory or MLCC spot prices begin moving in tandem, the notion of compute raw materials as a financialised asset class will have crossed from theory into reality.

*Key comparisons across Korea's three exposed companies:*

SK Hynix & Samsung Electronics (HBM/DRAM) — Role in compute: core components for processing and data handling. AI server content: multiple stacked HBM packages per unit. Supply: HBM4 in shortage; LTA adoption expanding. Pricing trend: HBM prices rising; LTAs intended to stabilise them. Market share: SK Hynix holds 50–61% of the HBM market. Opportunity from financialisation: wider long-term contracts, improved price visibility. Risk: amplified price volatility driven by speculative flows.

Samsung Electro-Mechanics (MLCC) — Role in compute: essential power-stabilisation component. AI server content: approximately 28,000 MLCCs per unit. Supply: lines at full capacity; Philippine expansion two years from production. Pricing trend: Murata-led price-increase discussions generating a sense of déjà vu with early DRAM cycles. Market share: approximately 40% of the AI server MLCC market. Opportunity from financialisation: product-mix improvement toward high-margin AI components. Risk: same speculative volatility transmission as memory.