SK Securities reiterated a buy recommendation on Hyosung Heavy Industries on the 16th, citing the company's expanding local production capacity in the American power infrastructure market, while trimming its target price to 4,000,000 won.

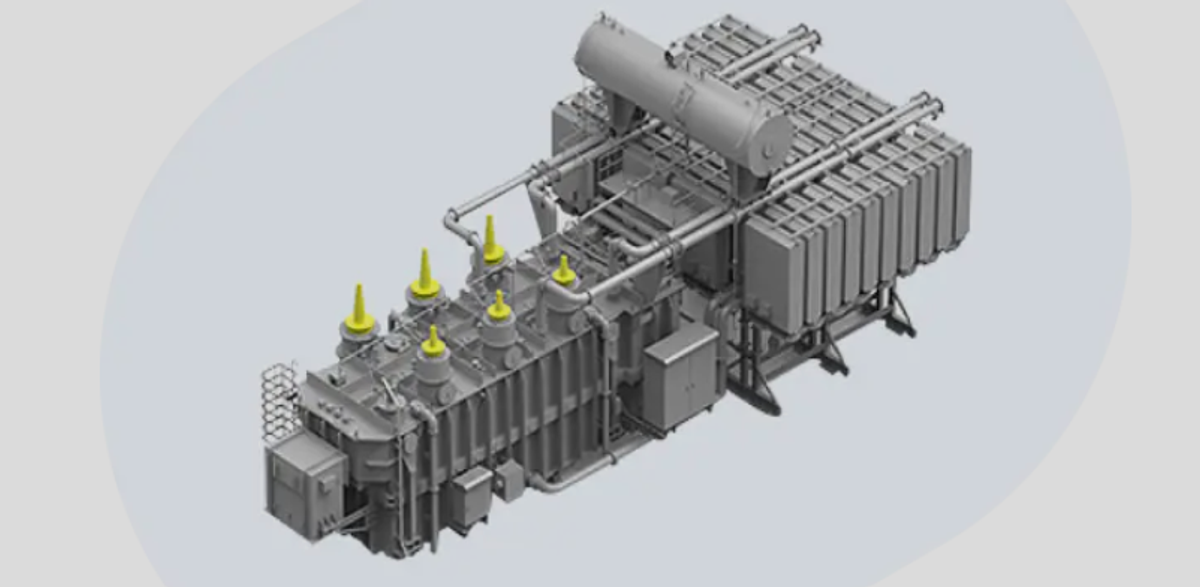

Hyosung Heavy Industries plans to establish a joint venture with Quanta Services, an American power infrastructure firm, to manufacture both transformers and gas circuit breakers (GCBs) on American soil. GCBs use insulating gas to achieve a compact form factor, enabling more efficient use of substation land.

Quanta Services anticipates structural growth in the 765kV transmission network market but has judged that its own production capacity alone is insufficient to meet domestic American demand at that voltage level — the reasoning behind its decision to partner with Hyosung, according to SK Securities.

The brokerage forecasts that Hyosung Heavy Industries' second-quarter 2026 results will meet market consensus. It estimates revenue of 1.936 trillion won and operating profit of 295 billion won for the quarter, implying an operating margin of 15.2%.

One potential complication is the risk of delays to certain Middle Eastern projects stemming from the US-Iran conflict. SK Securities noted, however, that Middle Eastern revenues account for just over 10% of total sales and are concentrated in Saudi Arabia; the brokerage therefore characterised any disruption as quarterly earnings noise rather than a structural risk.

Given that the company posted a record 4.2 trillion won in new orders in the first quarter, SK Securities said there is a good chance management will raise its full-year order guidance.

Hyosung's current share price of 2,677,000 won sits roughly 40% below its 52-week high of 4,601,000 won. SK Securities attributed the decline to supply-and-demand dynamics in the market rather than any deterioration in fundamentals, and described the stock as undervalued. The target price was reduced from 4,700,000 won to 4,000,000 won, implying upside of 49.4%.