Corporate leaders rarely stand before their own employees and say: "This is our fault." On 12th June, Han Jin-man, president of Samsung Electronics' foundry division, did precisely that. At an internal briefing on business performance, he told staff that management bore responsibility for the division's losses — and then delivered a number that will define Samsung's near-term narrative: the foundry business will not return to operating profit until 2028. That means another year of losses in 2027.

Six days later, on 18th June, Park Yong-in, president of the System LSI division — which designs chips such as application processors and image sensors — delivered an equally sobering message. Despite recording its highest-ever quarterly revenue in the first quarter of this year, he said annual operating losses remained unavoidable, owing to shifts in market demand. Record sales alongside unavoidable losses: that contradictory sentence captures precisely the structural trap in which Samsung's non-memory chip businesses now find themselves.

Two worlds under one roof

Samsung Electronics today contains two sharply different realities. Its memory division — buoyed by surging demand for high-bandwidth memory (HBM) chips used in artificial-intelligence servers, as well as conventional DRAM — is on track for another record quarter. Its non-memory operations, which comprise the foundry (contract manufacturing) and System LSI divisions, are expected to post a combined operating loss of between 2 trillion and 3 trillion won (roughly $1.5bn–$2.2bn) this year, following similar losses in 2024.

The divergence does not stay on the balance sheet. Under a bonus agreement recently reached with Samsung's union, employees in the Device Solutions (DS) semiconductor division will receive a special performance bonus equivalent to 10.5% of their base salary. However, 60% of the bonus pool is allocated separately to whichever DS units posted profits — this year, effectively the memory division. Staff in shared functions receive a rate roughly 70% of what memory employees collect. The cumulative effect, by some estimates, is a bonus gap of up to 540m won (roughly $390,000) between the highest-paid employees in Samsung's device business and the lowest-paid in its consumer electronics arm, and up to 390m won between departments within the DS division itself.

What makes this particularly corrosive is that employees had no say in which division they were assigned to. The same effort, at the same company, yields vastly different rewards depending on an administrative posting decision. Reports suggest that defections to rivals — including TSMC and SK Hynix — are already rising among foundry and System LSI staff. The two years between now and 2028 risk becoming, above all, years of talent haemorrhage.

Anatomy of a loss

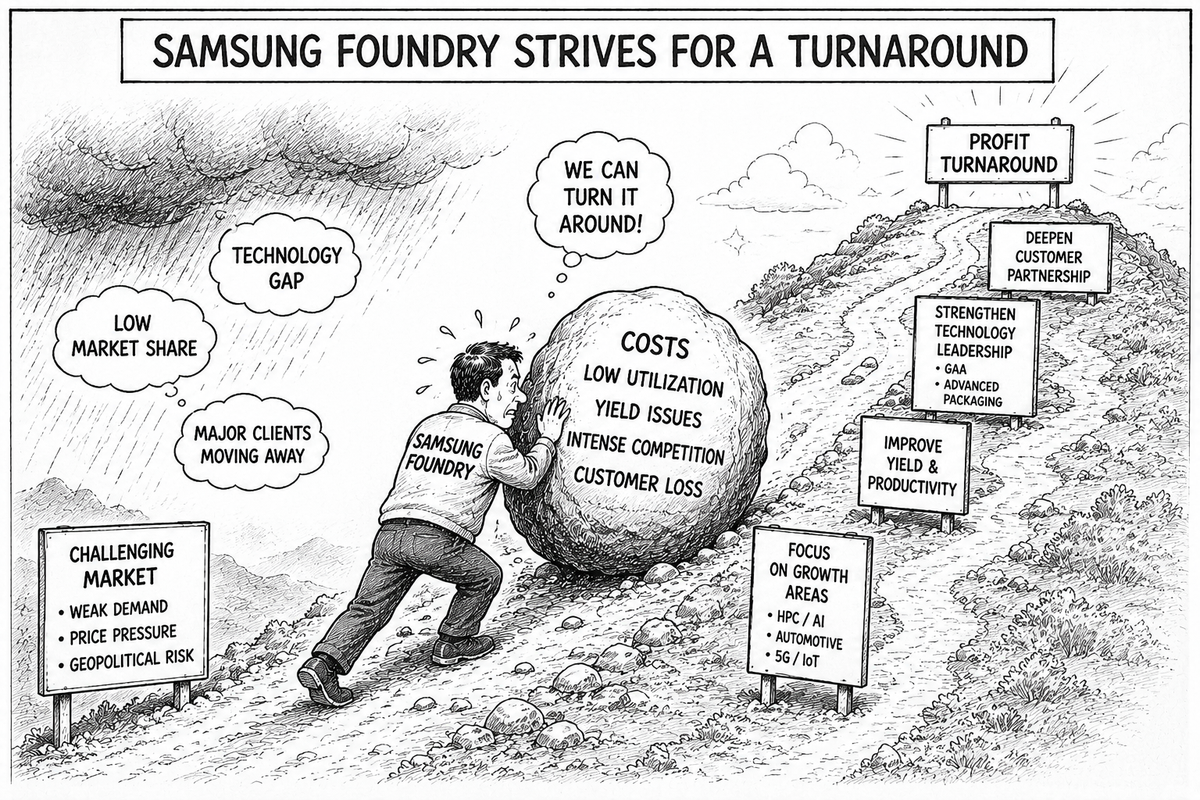

Mr Han was unusually candid about the causes. He identified four internal failures: Samsung was too slow to diversify away from smartphone chips; its process technology was insufficiently mature; it accepted unprofitable contracts to fill capacity; and it mismanaged its strategy for older, "mature-node" manufacturing lines. The additional cost burden from the newly agreed bonus scheme will, he acknowledged, extend losses into next year.

One of Mr Han's more striking announcements concerned Samsung's 8-inch wafer foundry business — a mature-technology line that is currently profitable. He said it was becoming a "red ocean" and signalled a gradual wind-down. Choosing to shrink a money-making operation is a deliberate bet on the future: Samsung is prioritising competitive position in cutting-edge processes over near-term loss mitigation.

Cards still in hand

The picture is not uniformly bleak. Yield rates on Samsung's 2-nanometre gate-all-around (GAA) process — the most advanced manufacturing technology it offers — have reportedly climbed above 60% in the first quarter of this year, a meaningful threshold for commercial viability. Older lines are busier: the sixth-generation HBM4 base die, chips for Nvidia's automotive processors, and components for a new Nintendo console processor are all in production, pushing up utilisation rates.

The most consequential contract in Samsung's pipeline is a reported $16.5bn (approximately 25 trillion won) agreement with Tesla to produce next-generation AI chips, known as AI6, at Samsung's 2-nanometre fab in Taylor, Texas — a plant expected to begin volume production next year. According to the Seoul Economic Daily, Samsung has also secured orders from Google, following earlier wins at Nvidia and Tesla, and plans to pursue business restructuring alongside performance improvement simultaneously. On 8th June, Samsung vice-chairman Jun Young-hyun formally confirmed that Nvidia's autonomous-driving chips would be manufactured at Samsung's foundry, underscoring the broadening of its blue-chip customer portfolio.

The central challenge of the next two years is bridging the gap between those future wins and the losses accumulating today.

What will sustain Samsung until 2028

Two things, ultimately, will determine whether Samsung can hold together long enough to reach its profitability target.

The first is cash from memory. As long as the HBM supercycle continues, the memory division's outsized profits can absorb the losses in foundry and System LSI, keeping the group solvent and funded for capital investment. That is the financial lifeline.

The second is people — and here the outlook is more uncertain. Management's public acknowledgement of its own mistakes is a necessary first step towards rebuilding internal trust. But candour alone will not prevent engineers from leaving if the structural pay disparity persists. Mr Han closed his address by telling employees that Samsung had "sufficient technology and capability to recover its competitiveness," and asking them to "trust each other and pull together." That a single sentence must carry both a declaration of confidence and an appeal for forbearance tells you a great deal about where Samsung's foundry division stands today.

The year 2028 is both a destination and a measure of endurance.

*Watch for: the quarterly trajectory of foundry and System LSI operating losses in the second half of 2026, and confirmation of Google's and other big-technology customers' orders. If losses narrow faster than expected, the 2028 target could yet be brought forward.*