Company Overview

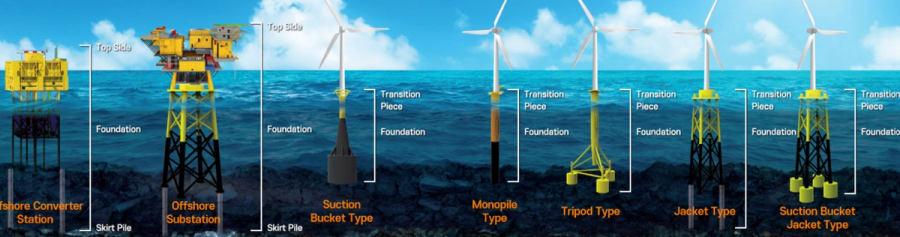

SK Ocean Plant is a specialist manufacturing and engineering firm within the SK Ecoplant group, focused on two core activities: fabricating substructures for offshore wind turbines (monopiles, jackets, and floating platforms) and providing maintenance, repair, and overhaul (MRO) services for offshore plant equipment. Operating from a production yard in Yeongam, South Jeolla Province, the company has expanded rapidly alongside South Korea's nascent offshore wind market and is now actively pursuing contracts in Europe and Taiwan as it seeks to establish itself as a global player.

On the Korean Stock Exchange (KOSPI), SK Ocean Plant is regarded as a bellwether for the offshore wind supply chain, particularly in structural and foundational components. The stock attracts attention from institutional and foreign investors given the South Korean government's renewable energy expansion targets, the global energy transition accelerated by the United States Inflation Reduction Act, and a surge in large-scale offshore wind procurement in Europe. Yet significant order-book volatility and lingering questions about whether annual revenues will breach ₩1 trillion (roughly $730m) mean that justifying its valuation against growth potential remains the central debate among investors.

The company's approach to value enhancement—known in Korean market discourse as "value-up"—is notably unconventional. Whereas large financial conglomerates and industrial firms typically boost shareholder value through dividend increases and share buybacks, SK Ocean Plant is pursuing a different path: securing earnings visibility, accumulating an order backlog, and engineering a rerating of the business. In practice, this means order momentum and improving profitability serve as the primary props for the share price, rather than direct cash distributions.

Business Profile and Financial Performance

Business Structure — A Single-Focus Portfolio Centred on Offshore Wind

SK Ocean Plant's operations fall into three categories: fabrication of offshore wind substructures (monopiles, jackets, and transition pieces); MRO services for offshore plant facilities; and a newer floating wind (floater) segment. Of these, substructure fabrication accounts for the overwhelming majority of revenues. The Yeongam yard has an annual production capacity of more than 100,000 tonnes of steel structures, making it one of the largest facilities of its kind in South Korea.

Expectations are also rising around a potential MRO contract for US military marine equipment. A market research report circulated in February 2026 suggested that the prospects for such a contract were becoming more concrete. Separately, the company is reported to be on the verge of securing contracts for a European offshore substation (OSS) project and Taiwanese offshore wind substructures. The prospect of diversifying internationally has become central to the company's medium-to-long-term growth narrative.

Financial Performance by Year

Year | Revenue (₩bn) | Operating Profit (₩bn) | Operating Margin (%) | Notes

2022 | c.420 | c.18 | c.4.3 | Early expansion of offshore wind market

2023 | c.580 | c.25 | c.4.3 | Domestic orders accelerate

2024 | c.850 | c.42 | c.4.9 | Delivery of multiple Taiwan and domestic projects

2025 | c.930 | 59.5 | c.6.4 | Record annual operating profit; ₩1 trillion revenue threshold in sight

*2025 figures are based on preliminary results disclosed by SK Ocean Plant in February 2026. Figures for 2022–2024 are estimates derived from publicly available data and may contain minor discrepancies.*

The 2025 operating profit of ₩59.5bn is understood to be the highest recorded since the company's founding. Revenue, approaching ₩1 trillion, is now widely regarded as a matter of timing rather than possibility. Equally encouraging is the improvement in the operating margin, which climbed to above 6%—a sign that the company is gradually escaping the notoriously thin-margin structure typical of heavy industrial fabrication.

Order Backlog and Growth Drivers

Europe's offshore wind market is targeting the installation of more than 20 gigawatts of new capacity per year by 2030, implying a structurally rising demand for substructures. SK Ocean Plant is understood to be simultaneously pursuing contracts for a European OSS project and Taiwanese offshore wind substructures in 2026. Should both be confirmed, the order backlog would expand substantially, providing strong revenue visibility for the following two to three years.

Key Value-Up Developments

February 2026 — Record Annual Results: Operating Profit of ₩59.5bn, Revenue Approaching ₩1 Trillion

On 2nd February 2026, SK Ocean Plant disclosed preliminary 2025 results showing annual operating profit of ₩59.5bn—growth of more than 40% year-on-year that reportedly exceeded market consensus. Revenue, in the high ₩900bn range, prompted widespread commentary that crossing the ₩1 trillion threshold was only a matter of time.

The announcement triggered a notable inflow of institutional buying. The strength of demand from fund managers was highlighted in market reports on 26th March 2026, when institutions were reported to have been net buyers of SK Ocean Plant in significant volume. This episode neatly illustrates the defining feature of SK Ocean Plant's value-up strategy: earnings visibility translates directly into share price momentum.

February 2026 — Overseas Order Momentum: Europe, Taiwan, and US Military MRO

An analyst report circulated on 24th February 2026 described SK Ocean Plant as being on the verge of securing both a European offshore substation contract and a Taiwanese offshore wind substructure order, while prospects for a US military marine MRO deal were said to be strengthening. Were all three to materialise, they would substantially improve both the size and quality of the company's order backlog.

This strategy of diversifying revenue sources away from the domestic market—rather than returning capital to shareholders through dividends or buybacks—reflects an approach to value creation in which the company's own growth story serves as the primary driver of shareholder value.

March 2026 — Share Price Surge: "Energy Highway" Policy Theme and a 30% Single-Day Gain

On 20th March 2026, SK Ocean Plant's shares hit the daily upper limit, rising 30%. The catalyst was policy enthusiasm surrounding the so-called "Energy Highway" initiative—a large-scale plan to build transmission and distribution infrastructure connecting offshore wind power to major onshore demand centres. Because this would directly stimulate demand for offshore wind substructures, the entire supply chain benefited.

The episode signals that the market has begun to reprice SK Ocean Plant not merely as a cyclical industrial stock but as a beneficiary of structural policy tailwinds. However, the sharp sell-off that reportedly followed the initial surge is a reminder that elevated volatility remains a persistent concern.

March 2026 — Annual General Meeting: Kang Yeong-gyu Appointed Chief Executive

At the annual general meeting held on 31st March 2026, shareholders approved the appointment of President Kang Yeong-gyu as the company's new chief executive. The change of leadership is interpreted as reflecting the SK group's commitment to accelerating international contract wins and business diversification. Markets are watching closely to see whether strategic continuity can be maintained through the management transition—a factor that matters considerably to the share price.

Challenges and Assessment

Challenges Ahead

First, achieving ₩1 trillion in revenue while simultaneously improving margins. Although the operating margin rose above 6% in 2025, this remains modest by any standard. Winning higher-value projects and achieving greater cost efficiency to push margins into double digits is an outstanding challenge.

Second, converting overseas order expectations into signed contracts. Markets appear to have priced in optimism around European, Taiwanese, and US military contracts. The share price is therefore exposed to sharp swings depending on the timing and scale of actual contract announcements. If expectations go unfulfilled, valuation pressures will intensify.

Third, articulating a shareholder returns policy. As yet, SK Ocean Plant has not publicly committed to specific dividend targets or share buyback and cancellation programmes. Once revenue growth and backlog accumulation reach a sufficient level, investors will almost certainly begin demanding a clear roadmap for cash distributions.

Fourth, consolidating the new management team. For overseas contract negotiations and domestic project execution to proceed smoothly, strategic continuity and organisational stability must be established under President Kang's leadership.

Assessment

SK Ocean Plant is widely regarded as possessing manufacturing capabilities within the Korean offshore wind supply chain that are difficult to replicate. Its record operating profit in 2025 represents meaningful validation of its growth narrative. The company is well positioned to benefit from the global energy transition—one of the most durable structural trends in capital markets today—which lends it genuine medium-to-long-term investment appeal.

That said, the absence of a shareholder returns policy and the recurring pattern of sharp share price swings driven by order speculation mean that the company has yet to fully embody the spirit of Korea's value-up initiative, which is aimed at resolving chronic undervaluation and improving returns to shareholders. SK Ocean Plant sits in an in-between stage: a growth-oriented value-up story with a conspicuous gap where the returns-oriented dimension should be.

Controversies and Limitations

No Shareholder Returns Policy — Growth Investment versus Cash Distribution

SK Ocean Plant has not publicly announced any target dividend payout ratio or plans to buy back and cancel shares. This stands in contrast to value-up leaders in comparable industries, which have built investor confidence through progressive dividends and buybacks. The company can reasonably argue that capital is better deployed in expanding overseas yard capacity, upgrading facilities, and investing in new business lines. Nevertheless, shareholders will inevitably press for clarity on when cash distributions might begin.

Order-Book Volatility and Share Price Swings — A Pattern of Short-Termism

As illustrated by the sharp reversal that reportedly followed the 30% surge on 20th March 2026, SK Ocean Plant's share price tends to overreact to policy momentum and order expectations. If the pattern of heavy institutional buying followed swiftly by profit-taking becomes entrenched, it risks eroding the confidence of long-term retail investors.

SK Group's Strategic Posture — Uncertainty from the Parent

Reports from January 2026 indicated that the SK group, South Korea's third-largest conglomerate (chaebol), has adopted a disposition favouring asset disposals over fresh investment across its portfolio companies, with the notable exception of SK Hynix, the memory chipmaker. Should SK Ecoplant—SK Ocean Plant's immediate parent—come under pressure from group-level asset rationalisation, capital support for SK Ocean Plant may be constrained. Uncertainty at the top of the ownership structure represents a structural risk to the subsidiary's value-up strategy.

Concentration Risk — The Double-Edged Nature of Offshore Wind Dependence

A revenue base concentrated in offshore wind substructures is a powerful advantage when the market is growing, but it also leaves the company exposed to project delays, order cancellations, or sudden spikes in raw material costs. Floating wind and US military MRO are emerging as potential new pillars, but their revenue contribution remains small. Portfolio diversification is very much a work in progress.

Key Metrics Summary

Year | Revenue (₩bn) | Operating Profit (₩bn) | Operating Margin (%) | Dividend Policy | Share Buybacks | Est. PBR

2022 | c.420 | c.18 | c.4.3 | Not disclosed | None | —

2023 | c.580 | c.25 | c.4.3 | Not disclosed | None | —

2024 | c.850 | c.42 | c.4.9 | Not disclosed | None | —

2025 | c.930 | 59.5 | c.6.4 | Not disclosed | None | —

*Dividend, buyback, and PBR data are unconfirmed from public disclosures. Revenue and operating profit figures for 2022–2024 are estimates.*

Key Event | Date | Detail

Record annual operating profit | February 2026 | Operating profit ₩59.5bn; revenue approaching ₩1 trillion

"Energy Highway" share price surge | 20 March 2026 | Share price up 30% in a single session

New chief executive appointed | 31 March 2026 | President Kang Yeong-gyu takes the helm

European OSS and Taiwan offshore wind contracts imminent | February–March 2026 | International order diversification momentum accelerates

Heavy institutional net buying | 26 March 2026 | Stock enters top institutional net-buy rankings