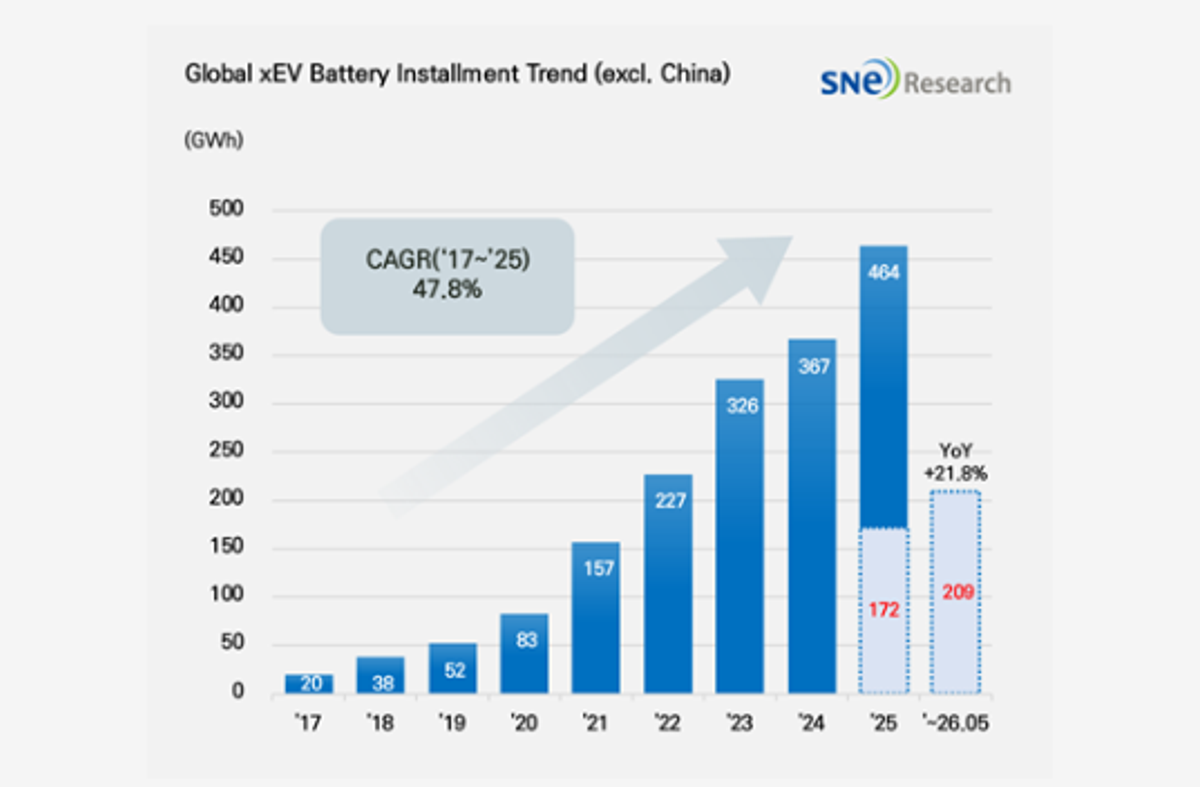

Global consumption of electric-vehicle batteries outside China reached 209.1GWh in the first five months of this year, up 21.8% on the same period in 2024, according to data published on 6th July by SNE Research, a South Korean energy consultancy. Chinese battery manufacturers are gaining ground swiftly in this market, while South Korea's three leading producers — LG Energy Solution, SK on, and Samsung SDI — have all lost share simultaneously.

CATL cements its lead with a 33.7% share

Contemporary Amperex Technology (CATL) consolidated its position as the top battery supplier outside China, recording usage of 70.6GWh — a 37.0% increase year on year. Its market share expanded from 30.0% to 33.7%. The company continues to broaden its supply across Europe, Asia, and emerging markets, counting Tesla, BMW, Mercedes-Benz, Toyota, and Kia among its customers.

LG Energy Solution holds second place but cedes 3.5 points

LG Energy Solution retained second position with 35.0GWh, a modest 1.0% increase in usage year on year. However, that growth fell well short of the overall market's expansion, causing its share to slip from 20.2% to 16.7%. The company continues to supply major carmakers including Tesla, General Motors, Hyundai Motor Group, and Volkswagen.

BYD surges 68.3% to claim third place

BYD recorded 22.2GWh, a 68.3% jump year on year, lifting its share from 7.7% to 10.6% and propelling it into third place. Growth was driven by rising overseas sales of BYD's own electric vehicles and an increase in supply to external customers.

Panasonic slips 8.5% on shifting Tesla demand

Panasonic's usage fell 8.5% year on year to 15.1GWh. Analysts attribute the decline to changes in the sales mix across Tesla's model range and softening demand in the North American market.

SK on and Samsung SDI both fall in volume and share

SK on recorded 15.8GWh, down 5.7% year on year, with its market share dropping from 9.8% to 7.6%. Steady sales of certain Hyundai Motor Group models were not enough to offset weakness among key customers Ford and Volkswagen, whose electric-vehicle sales have slowed.

Samsung SDI fared worse, with usage tumbling 29.7% to 8.7GWh and its market share more than halving from 7.2% to 4.1%. The company continues to supply BMW, Audi, and Rivian, but weak sales of Rivian vehicles in North America and declining volumes on legacy models translated directly into lower battery consumption.

Chinese challengers post triple-digit growth

Among smaller Chinese producers, Gotion recorded 7.8GWh (up 128.8%), SVOLT 6.3GWh (up 97.0%), and CALB 5.0GWh (up 77.5%). These companies are expanding their footprint outside China by riding the overseas advance of Chinese carmakers while competing aggressively on price with lithium iron phosphate (LFP) battery chemistries.

The combined market share of South Korea's three battery makers fell to 28.4%, down 8.7 percentage points year on year. Even as the ex-China market grew 21.8% overall, the Korean trio's aggregate volume actually declined — a stark illustration of how decisively the momentum has shifted towards their Chinese rivals.