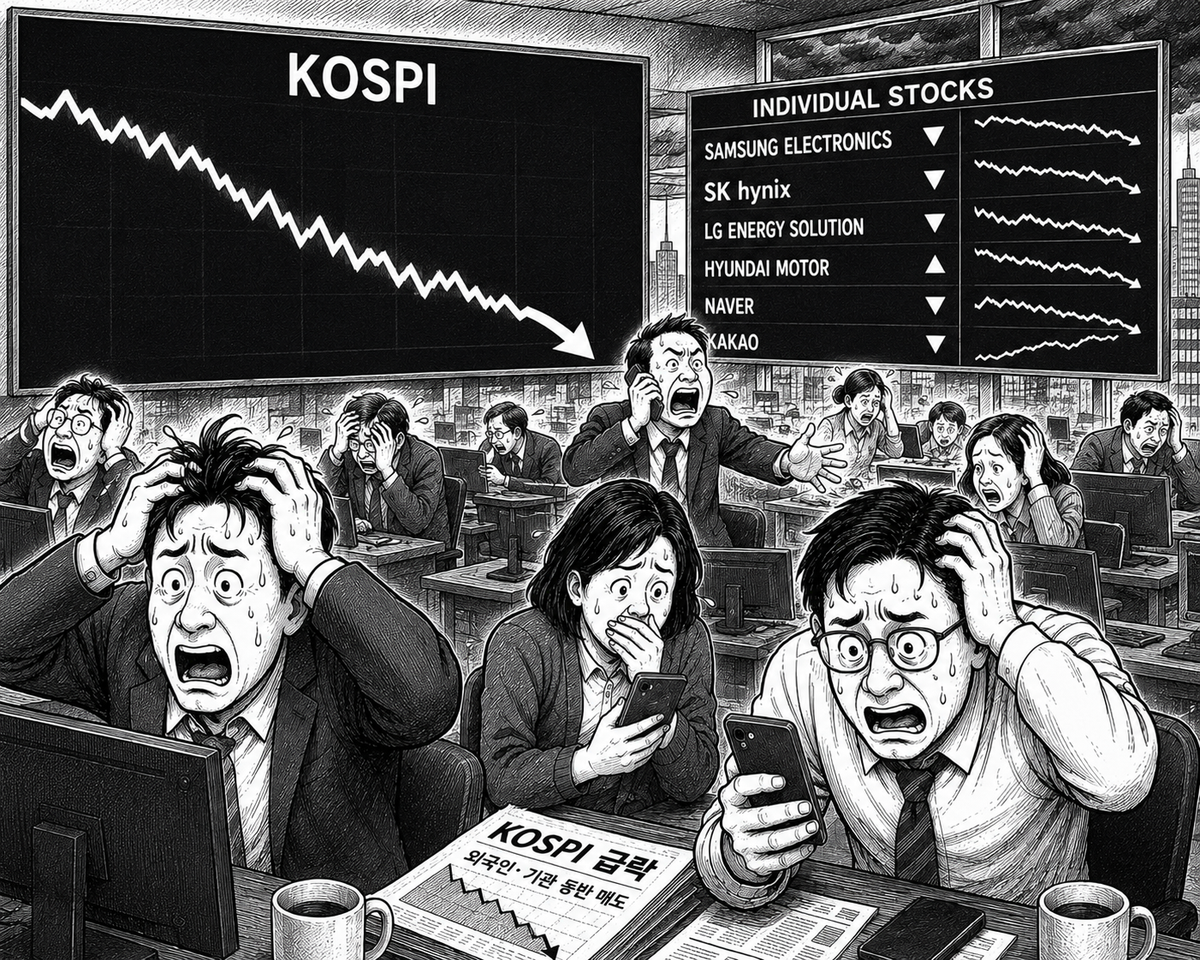

One number tells the whole story. On 23rd June, South Korea's benchmark KOSPI index closed at 8,203.84 — down 910.71 points, or 9.99%, from the previous session's 9,114.55. It was the largest single-day fall in the index's history. The secondary KOSDAQ tumbled 7.94%, while the KOSPI 200 shed 10.53%. Of the stocks that traded, 859 fell and just 46 rose. Foreign and institutional investors sold in concert; only retail buyers, absorbing more than 8 trillion won (roughly $5.8bn), kept the market from an even steeper collapse.

Financial analysts were quick to identify culprits. Three explanations dominated: caution ahead of earnings results from American chipmaker Micron Technology; South Korea's latest failure to win promotion to MSCI's developed-market index; and a renewed political row over taxing unrealised investment gains. Yet each explanation crumbles under scrutiny. Micron had not yet reported — the "caution" was speculative at best. The MSCI snub was widely anticipated and had been priced in across multiple review cycles. The tax dispute was nothing new. Can three such modest and familiar pieces of news, arriving together, plausibly produce the worst session in the KOSPI's recorded history?

The mismatch between catalyst and consequence

A better explanation lies in a structural shift in how volatile Korean equities have become. The market's baseline turbulence has ratcheted up: swings that would once have signalled a major turning point now feel almost routine. A 7% correction barely registers the alarm it once did. Seen through this lens, the June 23rd sell-off looks less like a response to fresh bad news and more like an acceleration of profit-taking that had already been building — with Micron's upcoming results providing a convenient excuse to act. The external triggers were real, but the finger on the trigger belonged to investors who had been sitting on substantial gains and waiting for a reason to sell.

Other evidence from the session supports this reading. Foreign investors were net sellers of KOSPI stocks for the second consecutive session, with their combined disposals of just two holdings — SK Hynix and SK Square — reaching 1 trillion won ($730m) alone. Waves of simultaneous profit-taking in semiconductor heavyweights visibly widened the intraday losses as the session progressed. This is entirely predictable behaviour: the stocks that have risen furthest are always the first to face the heaviest selling.

When the architecture of a rally becomes the machinery of a crash

There is a second structural force worth examining, one that had been flagged as a risk since at least May. The ETF-driven flows that powered the rally had, by design, channelled money with increasing concentration into Korea's two dominant semiconductor stocks. Bond-hybrid ETFs qualifying as safe assets within the country's retirement savings system were performing strongly. More strikingly, the underlying assets for South Korea's rare single-stock leveraged ETFs happen to be Samsung Electronics and SK Hynix — a coincidence that institutionalised the crowding of capital into precisely those two names.

The numbers are striking. During May alone, retail investors poured approximately 1.2 trillion won into a Samsung Electronics leveraged ETF and 2.7 trillion won into the SK Hynix equivalent. Total retail net buying of the two underlying stocks during the same month reached 9.6 trillion won and 15.8 trillion won respectively. Leveraged ETFs amplify gains twofold when their reference asset rises — but they amplify losses equally when it falls. The very mechanism that had intensified the rally instantly became an accelerant for the sell-off once prices began to turn.

The evidence that this mechanism fired on June 23rd is written plainly in the two stocks' closing prices. Samsung Electronics fell 12.31% to 310,000 won; SK Hynix dropped 12.47% to 2,555,000 won. Both declined significantly more than the KOSPI's already-punishing 9.99% average. The stocks that had risen the most fell the most.

A striking coincidence, but not a cause

One detail of timing is hard to ignore. The previous day, June 22nd, SK Hynix had briefly overtaken Samsung Electronics to become the KOSPI's largest company by market capitalisation — by a margin of 1.7474 trillion won — for the first time in 25 years and seven months. Precisely 24 hours later, the index posted its worst-ever daily loss. The observation made in May by analysts at Hana Securities — that an SK Hynix overtaking of Samsung's market cap could mark the end of the bull run — found a newly attentive audience.

Yet connecting this timing directly to the crash as cause and effect is a stretch. Of the five most-cited explanations for the sell-off — pre-Micron caution, the MSCI decision, the tax controversy, profit-taking, and leveraged ETF mechanics — none is "the market-cap reversal." What the reversal actually did was serve as a vivid symbol of a pre-existing condition rather than a new one. The spectacle of two enormous companies jostling for the top position was itself a mirror reflecting just how extreme the concentration of capital in those two names had become.

Healthy correction or something more worrying?

The consensus view in Seoul's financial community is that this was a compression of valuations, not a deterioration of fundamentals. Analysts point out that when the KOSPI fell 8.52% in a separate record-breaking session on June 8th, 12-month forward earnings-per-share estimates and operating profit forecasts barely moved. In other words, the market's expectations of what companies will earn remained intact; only the multiple that investors were prepared to pay for those earnings snapped back sharply. The same logic is being applied to June 23rd. With Micron's actual results still to come — and analysts' estimates likely to be revised upward in the aftermath — the prevailing view is that this is a violent but ultimately healthy recalibration of pace rather than direction.

That view may well prove correct. But the pattern itself demands attention. Within a single month, Korean equities suffered two separate falls in excess of 8% — events that each, in isolation, would previously have been considered historically extreme. Both episodes shared the same structural backdrop: ferocious concentration in two semiconductor stocks, a leveraged-product ecosystem designed to amplify that concentration, and a single piece of external news resting on top of the whole construction like a spark above a powder keg. If the news changes every time but the collapse looks the same, the true source of volatility is not the news. It is the structure.

What to watch: Micron's actual second-quarter results and the speed of the KOSPI's subsequent reaction. If the numbers come in ahead of expectations and the market continues to wobble, the case that this crash was structural rather than news-driven will become considerably harder to dismiss.

**Surface explanations (market consensus)** | **Deeper structural explanation**

Catalysts cited | Pre-Micron caution; MSCI exclusion; tax controversy | Profit-taking after a sharp rally; leveraged ETF amplification

Nature | External news and events | Internal market flows and architecture

Recurrence | Different news each time | Same pattern repeated (June 8th and June 23rd)

Evidence on the day | Micron had not yet reported | Samsung and SK Hynix both fell ~12%; retail leveraged-ETF net buying of 3.9 trillion won in May

Analyst conclusion | "Healthy correction"; "multiple compression, not earnings impairment" | Identical