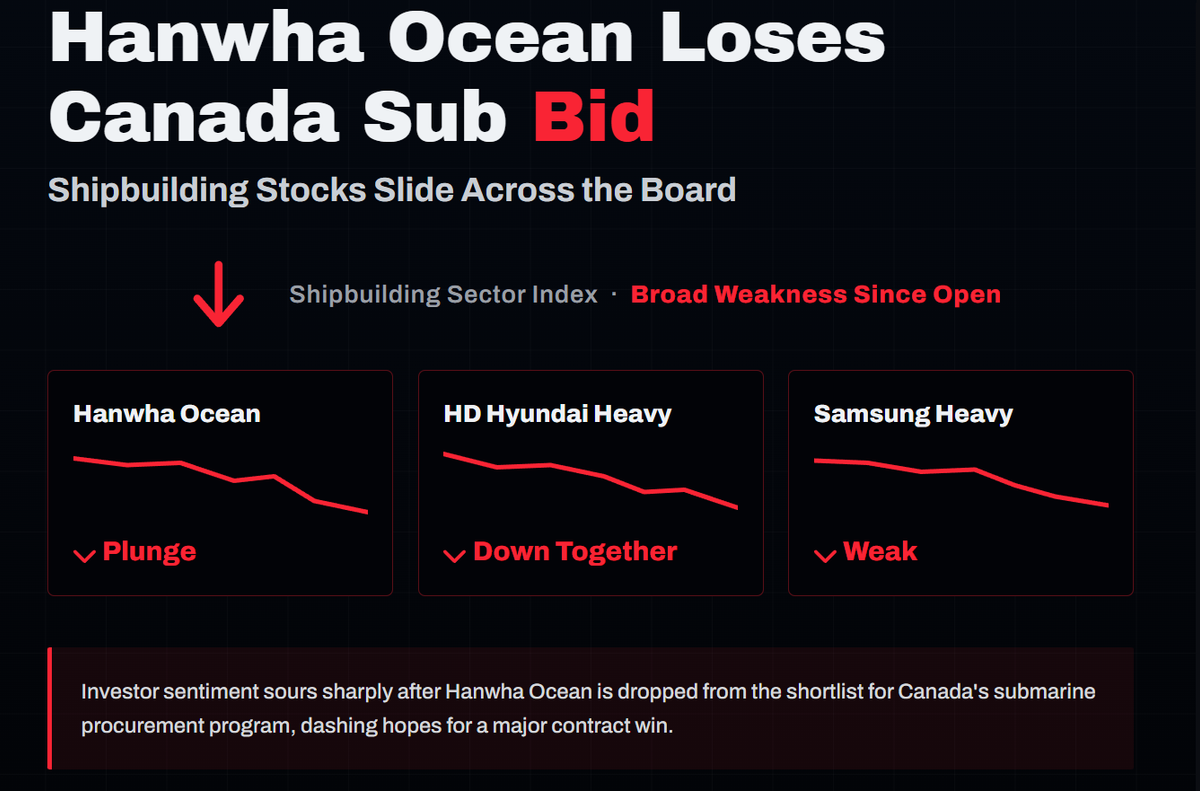

Hanwha Ocean plunged more than 20% after losing Canada's next-generation submarine contract to Germany. A simultaneous rout in semiconductor stocks dragged the wider market down by over 5%, but the true source of the shipbuilders' pain was the contract defeat itself.

*7 July 2026*

The three things you need to know

- Hanwha Ocean was eliminated from Canada's next-generation submarine programme (CPSP), worth up to ₩60 trillion, after the Canadian government selected Germany's ThyssenKrupp Marine Systems (TKMS) as its preferred bidder. On the day the news broke, Hanwha Ocean fell more than 20%, dragging down affiliated Hanwha Group companies and HD Hyundai Heavy Industries with it. - The same day, a sharp sell-off in Samsung Electronics and SK Hynix sent the KOSPI — South Korea's main stock index — down more than 5%, triggering a market-wide circuit breaker. Yet the shipbuilding and defence stocks fell far more steeply than the broader index, indicating that individual contract failure, rather than generalised risk aversion, was the primary cause. - Most analysts argue that the setback does not impair the underlying fundamentals of the shipbuilding industry. Order books in LNG carriers and commercial vessels remain robust, and Canada has reserved the right to reopen negotiations with Hanwha Ocean should talks with TKMS break down — meaning the door is not entirely closed.

Hanwha Ocean's shares fell more than 20% from the opening bell on 7 July, settling around ₩90,000 — down roughly 22% on the previous close — with losses even steeper in early trading. Affiliated Hanwha Group companies tumbled in sympathy: Hanwha Systems dropped about 16%, Hanwha Engine around 11%, and Hanwha Aerospace roughly 8%. HD Hyundai Heavy Industries, which had formed part of the consortium bidding alongside Hanwha Ocean, plunged as much as 10% at the open before recovering some ground. Samsung Heavy Industries, HD Korea Shipbuilding & Offshore Engineering, and other shipbuilding names also fell, leaving the entire sector badly shaken.

What happened

The trigger was an announcement by the Canadian government. Prime Minister Mark Carney confirmed on 6 July (local time) that TKMS had been selected as the preferred bidder for Canada's next-generation submarine programme — a contract encompassing the procurement of 12 diesel-electric submarines and 30 years of maintenance, repair and overhaul (MRO) services, with a combined value of up to ₩60 trillion (roughly C$60 billion). Had Hanwha Ocean won, it would have been the largest single defence export contract in South Korean history.

Hanwha Ocean had mounted an intensive campaign, forming a "One Team" consortium with the South Korean government and HD Hyundai Heavy Industries. The bid highlighted the proven combat record of the Chang Bogo-III submarine, delivery timelines faster than the competition, and pledges of more than US$70 billion in investment alongside the creation of an average of 25,000 jobs per year in Canada. South Korea's presidential chief of staff travelled to Ottawa personally to deliver a letter from the president. None of it was enough. The Canadian government's decision ultimately reflected a preference for NATO interoperability and European defence-supply-chain cohesion, analysts said. Prime Minister Carney himself acknowledged it had been "a very difficult and close choice between two highly qualified suppliers," and confirmed that both had met Canada's operational requirements.

Why the market reaction was so violent

The severity of the sell-off reflected how much of the contract win had already been priced in. On 6 July — the day before the announcement — Hanwha Ocean's shares had risen more than 9%, extending a four-session winning streak. When the outcome proved the opposite of what the market had anticipated, all of that accumulated optimism unwound at once.

There is broad agreement among analysts that the defeat was not a verdict on Hanwha Ocean's technical capabilities. Canada itself judged both bidders to have met its operational requirements; what separated them was geopolitics, not specifications. Germany's pitch leant heavily on NATO interoperability, North Atlantic security co-operation among Germany, Norway and Canada, and the broader context of European rearmament in response to the Russian threat. If that reading is correct, the outcome reflects the particular political dynamics of this specific procurement rather than any negative signal about South Korean submarine-building expertise.

A bad day made worse by semiconductors

The timing was particularly unfortunate. Samsung Electronics and SK Hynix — the two companies that between them dominate South Korea's technology sector — fell sharply on the same day, pulling the KOSPI down by more than 5% and triggering a circuit breaker during the afternoon session. That market-wide pressure doubtless added to the shipbuilders' losses. Even so, the gap between the index's decline and Hanwha Ocean's is revealing: the KOSPI fell roughly 5%, while Hanwha Ocean lost nearly four times that amount. Most other shipbuilding names also fell by more than the index. The semiconductor sell-off provided an unsettling backdrop, but the driving force behind the shipbuilding rout was unambiguously the Canadian contract defeat.

The fundamentals remain intact

Many analysts in Seoul's securities industry argue that the outcome should not prompt a wholesale reassessment of Hanwha Ocean's value — let alone the shipbuilding sector's. A single contract loss in one niche is not grounds for revising the broader investment case. Hanwha Ocean possesses world-class capabilities in LNG carriers and large container vessels, segments that are generating a steady stream of orders as LNG projects expand across the Middle East — including Qatar — and North America. The medium-term earnings outlook, anchored by a firm commercial order book and growing expectations for special-vessel exports, is unchanged. And because Canada has preserved the right to negotiate with Hanwha Ocean if talks with TKMS collapse, this episode may not be entirely over.

What next for shipbuilding stocks

Placed in its broader context, the sell-off takes on an additional layer of significance. In recent months, even as the KOSPI has risen sharply from its levels at the start of the year, shipbuilding stocks have conspicuously lagged the rally. Capital flooded into Samsung Electronics and SK Hynix to such an extent that the genuine improvements in order books and earnings among shipbuilders went largely unrecognised in their share prices — a theme explored in earlier articles in this series.

Against that backdrop, the Canadian-triggered sell-off admits two competing interpretations. The first is pessimistic: a sector already on the sidelines has now absorbed fresh bad news, and the defence-export narrative — which had commanded a premium within the shipbuilding story — has taken a meaningful knock. Recovery may take longer than it otherwise would. The second interpretation runs in the opposite direction. The core commercial fundamentals — LNG carriers, bulk vessels, container ships — are entirely unaffected by this episode. A sell-off that appears disproportionate to the underlying earnings outlook may simply represent a buying opportunity. Shipbuilding is a business defined by long-cycle order books, which afford unusual medium-term earnings visibility; short-term dislocations caused by single events need not dictate the sector's longer-run direction.

What to watch: Whether Canada and TKMS reach a final agreement — or whether negotiations break down and Hanwha Ocean gets a second chance. And, separately, whether LNG and commercial vessel orders continue to flow as expected, and whether follow-on contracts under the US-Korea shipbuilding co-operation framework (MASGA) materialise on schedule. The answers will determine whether last week's plunge proves a one-off shock or the beginning of a more prolonged period of underperformance.

**Factor** | **Detail**

Contract value | Up to ₩60 trillion (construction cost plus 30-year MRO); 12 submarines

Outcome | TKMS selected as preferred bidder; Hanwha Ocean eliminated

Stated reason for defeat | Geopolitical factors — NATO interoperability — rather than technical specification

Market impact | Hanwha Ocean –20%-plus; Hanwha Group affiliates and HD Hyundai Heavy Industries also fell sharply

Residual option | Canada reserves the right to reopen talks with Hanwha Ocean if TKMS negotiations fail

Fundamental impact | LNG and commercial-vessel order book and earnings outlook unaffected