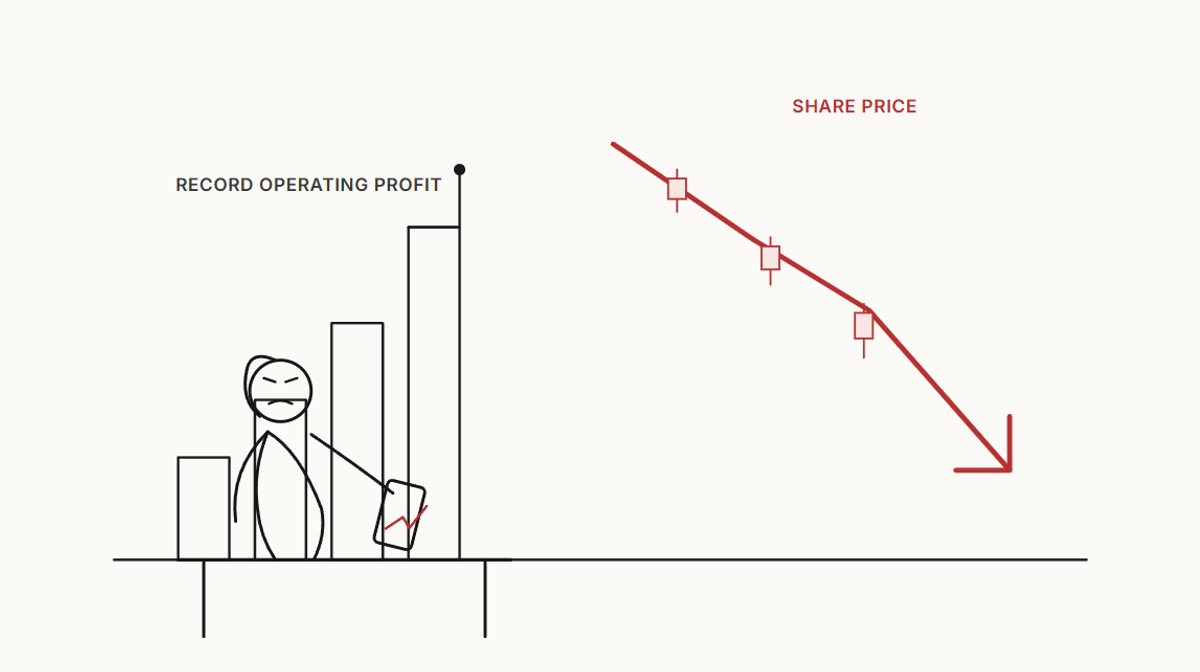

Operating profit of 89.4 trillion won, up 1,810% year on year, beating consensus. Yet Samsung Electronics shares fell nearly 9%. Five previous sell-offs this year have each ended with the index reaching new highs — and that pattern now poses the same question once more.

*7 July 2026*

The three things you need to know

- Samsung Electronics announced preliminary second-quarter results on the 7th: revenues of 171 trillion won and operating profit of 89.4 trillion won. Operating profit exceeded the market consensus of 84.6 trillion won, and the quarterly operating margin surpassed 50% for the first time in the company's history. Nevertheless, shares fell as much as 9% intraday, dragging down SK Hynix with them. The KOSPI (South Korea's main stock index) dropped to the 7,500 level, triggering a circuit-breaker in afternoon trading. - The problem lay not in the quality of the results but in the management of expectations. Revenues came in below prior estimates, stoking fears that the cycle had peaked. More fundamentally, the expectation of strong results had already been priced in — and when those results were confirmed, profit-taking selling flooded the market. - This is, however, already the fifth such correction this year. Each of the previous four ended without exception in new all-time highs. The geopolitical shock of March, and two separate sell-offs in June, all reversed within days to weeks. The KOSPI rose nearly 92% in the first half alone, repeatedly setting records.

On the numbers alone, this was a near-perfect scorecard. Samsung disclosed preliminary second-quarter revenues of 171 trillion won and operating profit of 89.4 trillion won. Operating profit rose 56% from the previous quarter and surged 1,810% year on year. The quarterly operating margin of 52% was the highest since the company's founding. Stripping out provisions for performance bonuses, underlying operating profit is estimated to have exceeded 106 trillion won — the highest of any global technology giant over the same period. Yet within moments of the announcement, Samsung's shares fell as low as 286,000 won intraday, a decline of roughly 9%. SK Hynix fell in tandem. The combined drop in the two stocks pushed the KOSPI below 7,500, and a circuit-breaker was triggered during the afternoon session.

Why stellar results became a reason to sell

The phrase most frequently heard from brokers was "sell-on-news." The analysis is straightforward: Samsung revealed record-breaking results, but the catalyst had already been consumed. The market had effectively known these numbers were coming. Micron Technology's strong recent results had led investors to expect a bumper quarter from South Korean chipmakers, and that expectation had already been absorbed into share prices over the preceding months — a point on which brokerage analysts were unanimous. The steady upward creep in price targets in the weeks before the announcement was itself evidence that optimism had been front-loaded.

The revenue miss then ignited fears that the cycle had peaked. Although operating profit beat consensus, revenues of 171 trillion won fell short of prior estimates, triggering what analysts described as a vague but powerful anxiety about peak earnings. Investors were less interested in the absolute size of the profit than in the question of how much longer this growth trajectory could be sustained. Bloomberg noted that with much of the bullish case already reflected in valuations, investors were treating the strong results not as a signal to buy more but as an opportunity to reduce exposure.

A familiar pattern

Taken in isolation, this looks alarming. But a review of the KOSPI's behaviour this year yields a different conclusion. This is already the fifth episode this year in which the index has fallen sharply — by roughly 8% — in a single session. There were two such drops in early March, triggered by geopolitical tensions between the United States and Iran, and two more in early and late June, driven by concerns over memory chip demand and earnings caution. Each time, the recovery was swift, and each correction ultimately gave way to new highs.

The sell-off on 8 June is illustrative. The KOSPI fell more than 8% intraday that day, triggering both a circuit-breaker and a sell-side sidecar (an automatic curb on index futures trading). Samsung Electronics briefly fell below 300,000 won and SK Hynix below 2,000,000 won — psychologically significant thresholds for Korean investors. The very next trading day, a rebound in US semiconductor stocks and a 5.61% surge in the Philadelphia Semiconductor Index pulled Korean equities sharply higher, this time triggering a buy-side sidecar. Samsung recovered 8.97% in a single session; SK Hynix surged 15.91%, erasing most of the previous day's losses.

Lee Jae-won, an analyst at Yuanta Securities, noted that since 2000 there have been only seven occasions on which the KOSPI has fallen 8% or more in a single day, and that outside the 2008 global financial crisis, meaningful recoveries have followed in virtually every instance. Yuanta's data show that in the aftermath of such drops, the KOSPI has delivered average returns of 5.5% over 10 trading days, 6.5% over 30 trading days, and 15.3% over 90 trading days.

The period following the late-June correction produced an even more striking rally. SK Hynix repeatedly set 52-week highs throughout June, breaking through 2,700,000 won on 18 June and surpassing 2,800,000 won in pre-market trading the following day — in the process overtaking Micron's market capitalisation. On 23 June, SK Hynix briefly surpassed Samsung Electronics in market capitalisation, becoming the largest company on the KOSPI by that measure for the first time in 26 years. The KOSPI index itself surged 91.9% from 4,214.17 at the start of the year to 8,088.34 at the end of the first half, and on 19 June hit an intraday record of 9,385.59. Each time a correction prompted fears that the rally had finally broken, it instead proved to be a platform for yet another advance.

Will this time be different?

There is no shortage of reasons to believe the pattern will repeat. Crucially, the underlying earnings trajectory has not been called into question. Eugene Investment and Securities forecasts Samsung's full-year operating profits at 361.3 trillion won for 2025 and 589.4 trillion won for 2026. It has also been confirmed that negotiations are under way to raise average selling prices for DRAM and NAND flash memory by more than 20% in the third quarter. Daeshin Securities raised its price target for SK Hynix to 3,900,000 won on the day of the sell-off; SK Securities and Mirae Asset Securities have similarly maintained buy recommendations on both stocks, arguing they remain undervalued relative to sector peers.

Valuations reinforce that view. The KOSPI's forward price-to-earnings ratio has fallen to 6.4 times — its lowest level since the global financial crisis — which, for many analysts, suggests that today's decline was excessive and irrational. Several brokers are recommending that investors hold rather than sell, interpreting the drop not as a response to disappointing fundamentals but as the unwinding of speculative positions accumulated during recent dips. The expectation is that once this profit-taking is absorbed, the upward trend will reassert itself.

Yet caution is also warranted. This correction has a distinguishing feature absent from the previous four: for the first time, it was triggered partly by the company's own reported numbers — specifically, a revenue figure that missed expectations. The prior four sell-offs were each driven by external factors: geopolitical risk, macro caution, the failure to secure index inclusion. None called into question Samsung's or SK Hynix's actual results. That one element of those results — revenue growth — has now disappointed makes it harder to conclude with confidence that this correction is identical in nature to those that preceded it.

What to watch: Whether this correction follows the established script and gives way to new highs within days or weeks — or whether slowing revenue growth is confirmed by successive data points, making this the first correction of a genuinely different character. The first clues will come from Samsung's third-quarter guidance, due in early August, and from SK Hynix's second-quarter results, scheduled for 29 July.

*Summary of 2026 corrections to date*

Date | Apparent trigger | Outcome

Early March | US-Iran geopolitical risk | Recovered; first-half rally followed

8 June | Memory pricing concerns; fears of slowing big-tech investment | Buy-side sidecar next day; Samsung +8.97%, SK Hynix +15.91%

23 June | Micron earnings caution; MSCI inclusion failure | SK Hynix became KOSPI's largest company by market cap; new highs followed

26 June | Memory demand slowdown fears | KOSPI subsequently hit all-time high of 9,385.59

7 July (current) | Revenue miss; sell-on-news after front-loaded expectations | Under observation — earnings direction intact; price targets continue to rise