Markets sometimes react to distant events with startling speed. When reports emerged that Iran had extended its military reach beyond the Strait of Hormuz into the broader Persian Gulf, international oil prices jumped to a 20-month high. The shockwave crossed the Pacific and landed squarely in Yeouido, Seoul's financial district. The logic was straightforward: prolonged high oil prices would drive demand for alternatives such as solar and wind power. Hanwha Solutions surged 16.67%; HD Hyundai Energy Solutions hit its daily limit-up. Wind-energy plays SK Oceanplant and CS Wind rose 9.42% and 11.83% respectively.

A second trigger compounded the move. Analysts began speculating that the Trump administration might decline to appeal a court ruling that had struck down its moratorium on offshore wind development. Bank of America described the situation as "progressing in a positive direction." A White House that had spent months hobbling the wind industry appeared, under the pressure of war-driven energy prices, to be softening its stance.

Then, the following day, much of those gains were surrendered. The pattern is familiar. News-driven waves crest quickly and recede almost as fast once the excitement fades. The more important question is what remains once the wave has passed. The answer lies not in price charts but in financial statements.

SK Oceanplant: selling less, earning more

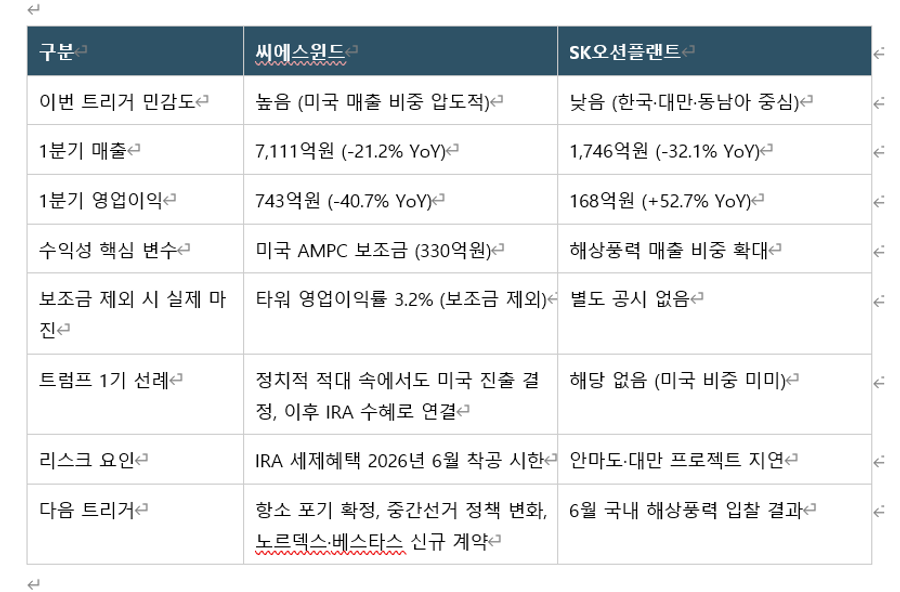

SK Oceanplant's first-quarter results reveal an intriguing asymmetry. Revenue fell 32.1% year-on-year to 174.6 billion won. Yet operating profit rose 52.7% to 16.8 billion won. The company sold less and earned more.

The explanation lies in the revenue mix. The operating margin expanded from 7.9% in the fourth quarter to 9.7% in the first quarter, driven by a higher proportion of offshore wind business. Moon Gyeong-won, an analyst at Meritz Securities, attributed this to "strong offshore wind margins" and raised his target price by 15.4%, from 26,000 won to 30,000 won. The offshore wind substructure business is generating better returns than the group's traditional shipbuilding and plant operations — a sign that the company's portfolio is quietly rebalancing.

Shadows remain, however. A contract for the Anmado offshore wind project, which had been expected to contribute to fourth-quarter revenues, was cancelled amid uncertainty over a military operational assessment. A Taiwanese project, the Weilun offshore wind farm, has been delayed after its developer revised its investment decision. Mirae Asset Securities has cut its 2026 revenue forecast for SK Oceanplant by 7%, to 699.8 billion won. First-quarter order intake came in at just 114.6 billion won — comprising 106.2 billion won from offshore wind and 8.4 billion won from maintenance, repair and overhaul work — leaving an order backlog of roughly 1.2224 trillion won. Positives and negatives are packed into a single quarter.

Crucially, SK Oceanplant's business is spread across South Korea, Taiwan and South-East Asia; its exposure to the American market is limited. The immediate trigger — the prospect of the Trump administration abandoning its appeal — has little direct bearing on this company's fundamentals. The more important story lies elsewhere.

CS Wind: the real beneficiary

CS Wind, the world's largest wind-tower manufacturer, presents a more complex picture. First-quarter revenue fell 21.2% year-on-year to 711.1 billion won, while operating profit dropped 40.7% to 74.3 billion won. An operating margin of 10.4% looks reasonable on the surface.

But when Jeong Yeon-seung, an analyst at NH Investment Securities, dug deeper, a different picture emerged. Buried within that operating profit figure is 33 billion won in subsidies from the Advanced Manufacturing Production Credit (AMPC), a tax incentive under America's Inflation Reduction Act (IRA). Strip that out and the underlying operating margin on actual tower manufacturing falls to just 3.2% — below market expectations. CS Wind's profitability, in other words, owes more to American government policy than to its own competitive edge in manufacturing.

That dependency creates direct political risk. The AMPC is grounded in the IRA, and the Trump administration has maintained a general posture of rolling back clean-energy tax incentives. Wind and solar projects must break ground by 30th June 2026 and begin commercial operations by 31st December 2027 to qualify for existing credits. Projects announced after those deadlines may fall into a subsidy vacuum.

Even so, some analysts are cautiously optimistic. Cho Jae-won at Kiwoom Securities argues that expanded production and productivity improvements at CS Wind's American operations should begin feeding through from the second quarter onwards — suggesting that margin recovery may increasingly be self-generated rather than subsidy-dependent. Jeong at NH Investment Securities notes that the company secured $230m in new orders during the first quarter, achieving 13.4% of its annual target, and considers the order pipeline broadly manageable. The pivotal variable, he argues, is whether CS Wind can land new long-term supply agreements with turbine makers Nordex and Vestas; negotiations are expected to conclude in June, and the outcome could serve as the first catalyst for a meaningful re-rating.

A familiar pattern: rhetoric and reality diverged before

A longer view of the policy landscape around CS Wind reveals an instructive precedent. Throughout Donald Trump's first term (2017–2021), the White House was openly hostile to wind power. Mr Trump pursued litigation all the way to the UK Supreme Court over an offshore wind farm near his Scottish golf course and attacked wind turbines on Twitter more than 60 times during his presidency. "Wind kills birds and ruins landscapes" became something of a trademark line.

Yet the American wind industry's actual trajectory ran in precisely the opposite direction. In 2018, the United States installed 7,588 megawatts of new wind capacity — the third-highest annual total on record and 8% more than in 2017. GE's wind-turbine order intake reached a then-record 4,206 units in 2019, up 32% year-on-year. While the federal government's rhetoric was hostile, the industry quietly thrived on falling costs and growing private-sector demand. Political posturing and industrial fundamentals moved in opposite directions.

CS Wind placed its American bet in exactly this context. The company began publicly pursuing US market entry in 2020 and, in June 2021 — near the end of Trump's first term — acquired Vestas's American wind-tower manufacturing plant. That wager subsequently caught the tailwind of the IRA, giving rise to the very AMPC subsidy income that now underpins its earnings.

Comparable dynamics may now be reasserting themselves. Mr Trump's approval ratings are sliding, and midterm elections loom in November. The administration's apparent willingness to drop its court appeal can be read as a signal that, with its political capital diminishing, it is reluctant to pick unnecessary fights. As in the first term, the gap between governmental rhetoric and industrial reality may narrow — and, when it does, close in the industry's favour.

There are, however, meaningful differences from the first term. This time, a concrete subsidy framework — the IRA — already exists and has itself become a political battleground. The 30th June 2026 construction deadline introduces a specific, time-sensitive pressure that was absent before. Still, one thing is clear: under Trump administrations, what Washington says about wind power and what the wind industry actually does have repeatedly diverged.

Two companies, one conclusion — but the weight falls unevenly

SK Oceanplant and CS Wind operate different businesses, but their situations point to the same broad conclusion: current earnings are, in essence, numbers produced during a period of transition. When it comes to this particular trigger, however, the balance of relevance tilts sharply in one direction. SK Oceanplant's fortunes are tied chiefly to permitting risks in South Korea and Taiwan; CS Wind is directly exposed to shifts in American policy. If the Trump administration's retreat on offshore wind, the constraints imposed by falling approval ratings and the arithmetic of midterm elections all align in the same direction, the company that stands to benefit first and most is CS Wind.

The real inflection points are in June — not the Middle East

High oil prices driven by an Iran–US military confrontation are a tailwind for wind energy, but a volatile one. When the conflict eases, energy prices will fall, and the narrative that propelled wind stocks will dissipate with them. The inflection points that genuinely merit investor attention lie elsewhere.

The first is South Korean government policy on offshore wind. The Ministry of Climate, Environment and Energy has this year tendered approximately 1,400 megawatts of fixed-bottom and 400 megawatts of floating offshore wind capacity in a competitive auction. This forms part of a broader roadmap allocating 7–8 gigawatts across three auction rounds between late 2024 and the first half of 2026. When results are announced in June, the pipeline of work for domestic substructure manufacturers — including SK Oceanplant — over the following two to three years will come into sharper focus.

The second is the underlying productivity of CS Wind's American operations. The key question for the next one to two quarters is whether manufacturing margins improve on their own terms, independent of AMPC subsidies. The company's existing project portfolio provides a degree of earnings visibility through the third quarter of 2027, but sustainability beyond that point depends on new orders.

Waves made by geopolitical events surge and recede quickly. But slower-moving variables — auction results, productivity metrics and political approval ratings — reveal the true shape of the wind industry more gradually and more honestly. Right now, the weight of those slower variables is tilting towards the company with the largest exposure to the American market.

Watch for: confirmation of whether the Trump administration formally drops its offshore wind appeal; any shift in clean-energy policy ahead of November's midterm elections; and the outcome of CS Wind's long-term supply contract negotiations with Nordex and Vestas. Should all three align, the pattern of Trump's first term — in which the gap between political rhetoric and industrial growth eventually closed in the industry's favour — may well repeat itself.